The Best Performing Alcohol Categories in 2024

2024 has been a challenging year in the alcohol category. While beer and wine have both seen declines, spirits have managed to achieve positive growth in value (+0.3) and volume (1.7%) for the 52 weeks ending August 10, per a recent Nielsen IQ webinar. However, said growth was driven solely by RTDs, as removing these from the category’s off-premise performance reveals a 0.4% volume loss for the same period.

Where Are Alcohol Consumers Shopping?

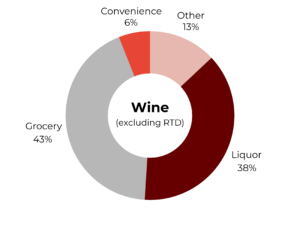

Consumers are choosing to shop at familiar channels that offer them value for money and convenience. The convenience store channel is driving quite a bit of growth, increasing its dollar sales by 1% compared to a year ago. Mass merchandise stores and dollar clubs are also performing well as a group, increasing dollar sales by 0.4%, while liquor stores and grocery stores have both seen a decline in sales so far this year.

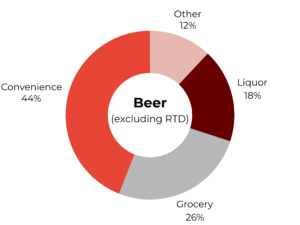

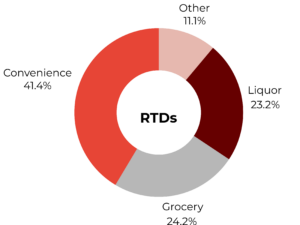

The strong performance of the convenience channel is driven by RTDs and beer, as these locations offer a friction-free environment to quickly and easily purchase these categories. With consumers showing an inclination to shop both close to home and in close proximity to the time of consumption, the familiarity and ease of convenience stores have made them a go-to. 41% of all RTD purchases off-premise occur in convenience stores- more than any other channel.

Convenience is such a driving force that C-stores are actually growing via all of the spirits, wine, and RTD categories. Recent developments in spirits-based RTD legislation have made the category increasingly available in C-stores, contributing to a loss in volume for open-state liquor stores.

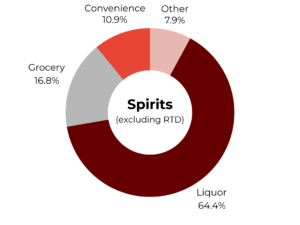

But make no mistake—for spirits, the liquor store is still the preferred shopping destination. On the whole, liquor stores claim a 65% share of off-premise purchases for the spirits category (excluding RTDs), where consumers appreciate the variety and selection-driven nature of these locations. Grocery stores and convenience stores are the next two most shopped locations for spirits, claiming 17% and 11% shares, respectively.

To combat some of the losses in U.S. liquor stores, there has been an increase in promotions and discounts, bringing the average price per unit down 1.4% between January 2023 and August 2024. The goal is to drive foot traffic and get people in the door. Yet, certain categories in the liquor store channel remain significant opportunities to target. Non-alcoholic spirits, wine cocktails, spirits-based RTDs, and Tequila are all strong growth drivers in the liquor channel, while hard seltzers, wine, rum, and cognac are seeing the most significant category declines within the liquor store channel.

Dollar Share by Channel

Source: Nielsen IQ

Alcohol Trends in Key States in 2024

In California, the largest beverage alcohol market in the United States, spirits-based ready-to-drink cocktails have seen 37% growth compared to one year ago. This market tends to stay ahead of the curve for emerging flavors as well. It’s also one of the strongest markets for the tequila category, with 27% of all spirits dollars spent in the state dedicated to the tequila category.

Texas is among the more interesting off-premise markets, as categories that have struggled nationwide have found pockets of growth within the state. This is particularly true with cognac, which has grown by 2% in the state as opposed to one year ago. The same can be said for below-premium beer, which is up 6%. The agave spirits and spirits-based cocktail segments each showed 8% growth compared to one year ago.

Off-premise stores in New York have an extensive depth of selection within the wine category and whiskey subcategory. There are more than 30k wine UPCS in the state. Although whiskey is the number one spirits category in New York, it has lost ground to Tequila and Mezcal which have grown a combined 4% across off-premise liquor stores. The state is home to an outsized number of high-volume spirits stores that have an emphasis on a diverse selection of spirits items.

Meanwhile, in New Jersey, some spirits categories that are seeing national declines are trending positively. Brandy and rum, for example, have grown by 5% and 4%, respectively. New Jersey’s liquor store channel has been particularly profitable for RTD spirits cocktails which have grown by 24%.

In Florida, the categories that are out of favor according to national data but have found pockets of growth include whiskey, which has seen a 3% increase year-over-year in the state. Likewise, still wine is doing quite well in Florida’s liquor store channel, offering 2% growth through August 10. Due to the notable influence of Hispanic culture in the state, the state has become one of the largest opportunities for agave spirits brands. Tequila and mezcal have seen an impressive growth rate of 15% year over year while imported beers have also increased by 4%.

More Resources on Alcohol Category Trends

A Comprehensive List of New Alcohol Products in 2024